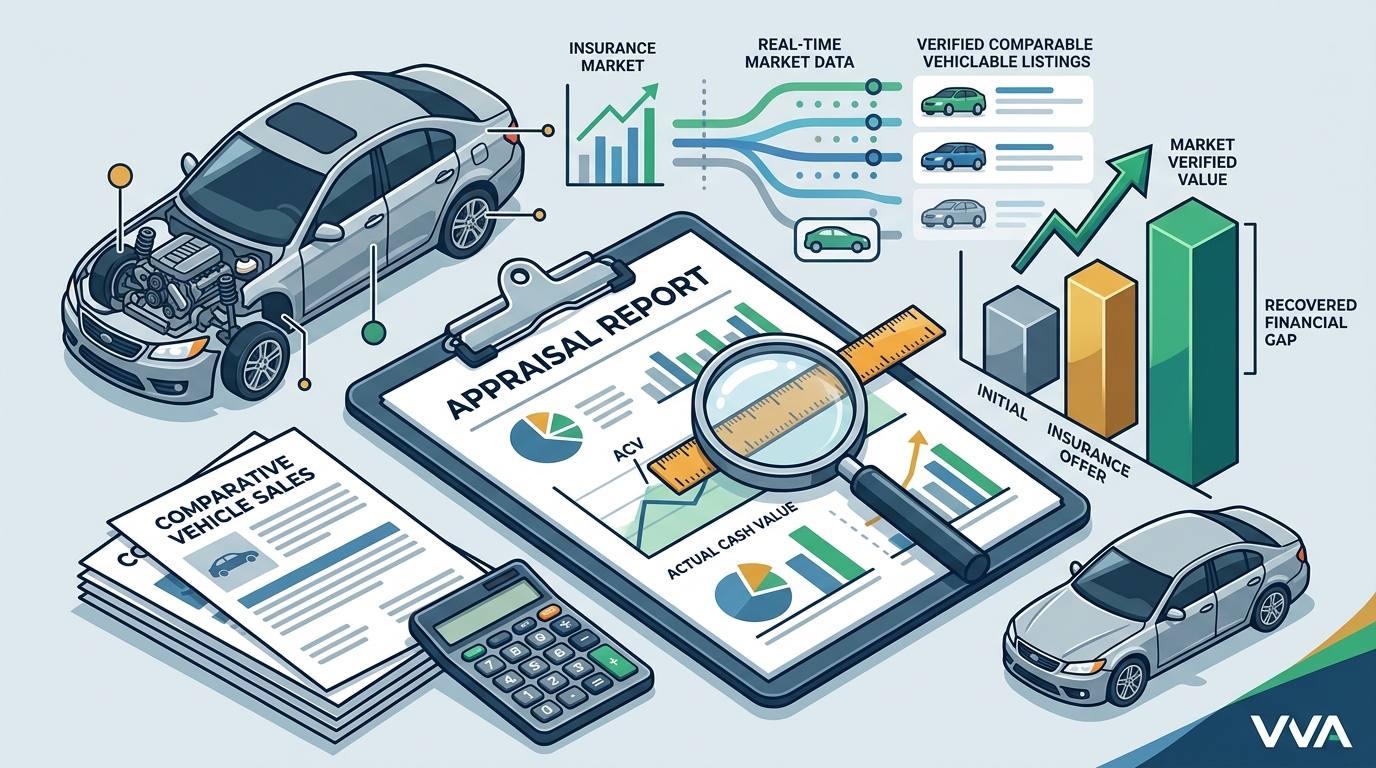

When your vehicle is damaged in an accident, the insurance company’s initial offer rarely reflects the true market reality. According to recent industry data, insurers frequently undervalue property damage claims by an average of 15 to 20 percent, leaving vehicle owners with significant financial gaps. This discrepancy occurs because insurance adjusters rely on proprietary algorithms rather than real-time comparable sales data. To recover the full value of your pre-loss asset, you need a valuation partner that uses verified market evidence, not just estimated lists. (Vehicle Valuation Services for)

Understanding Actual Cash Value vs. Market Value

Before engaging a valuation expert, it is critical to distinguish between the terms insurance carriers use and the terms the market uses. Actual Cash Value (ACV) is defined as the fair market value of your vehicle immediately before the loss occurred, minus depreciation. This definition is standard across the insurance industry but is often applied loosely by adjusters.

Diminished Value is the loss in market value that remains even after your vehicle has been perfectly repaired. This concept is vital for total loss scenarios or severe repairs where the vehicle’s history permanently affects its resale price. Inherent Diminished Value specifically refers to the loss in value due to the accident history itself, regardless of repair quality.

Vehicle Value Analysis provides a bridge between these concepts. They do not rely on generic book values. Instead, they utilize real comparable sales data to establish what buyers are actually paying for similar vehicles in your specific geographic region. This approach ensures that the pre-loss value is grounded in reality, not theoretical models.

Why Insurance Estimates Are Often Inaccurate

Insurance adjusters are trained to minimize payouts. They often use software that pulls data from national databases, which can lag behind real-time market fluctuations. For example, during periods of high demand for used cars, algorithmic estimates may fail to capture the sudden spike in value for specific makes and models.

Furthermore, these systems often ignore local market nuances. A vehicle that is highly valued in one region may have a lower valuation in another due to supply and demand dynamics. Without access to local comparable sales, the pre-loss value calculation becomes a guess rather than a fact. This is where independent valuation becomes essential for protecting your financial interests.

According to data from the National Highway Traffic Safety Administration (NHTSA), damage classification and total loss thresholds are complex and vary by state regulations. Navigating these regulations requires expert knowledge that general adjusters may lack. Vehicle Value Analysis leverages over a decade of Texas market data and national comparable sales to provide reports that are recognized by major insurance carriers.

The Methodology Behind Accurate Valuations

The core differentiator for Vehicle Value Analysis is their commitment to real comparable sales. They do not use estimates. Their process involves identifying vehicles that were sold recently, in close proximity to your location, and with similar specifications to your pre-loss vehicle.

This methodology provides a defensible deviation-percentage formula that can be used in negotiations or appraisal clauses. The resulting report includes a verified comparable sales grid, which serves as irrefutable evidence of your vehicle’s true market value. This level of detail is rarely available in standard insurance estimates.

Loss of Use is another critical component often overlooked. This refers to the compensation for the inability to use your vehicle while it is being repaired or replaced. Vehicle Value Analysis provides comprehensive Loss of Use Reports that calculate the daily rental cost and duration, ensuring you are not out of pocket for transportation during the claim process.

Comparing Silver, Gold, and Platinum Reports

Vehicle Value Analysis offers tiered reporting options to suit different needs, from individual policyholders to large law firms. Understanding these tiers helps you choose the right level of support for your specific claim.

| Report Tier | Best For | Key Features | Delivery Time |

|---|---|---|---|

| Silver Report | Individual Policyholders | Free initial assessment, basic market value range | Instant |

| Gold Report | Severe Damage Claims | Full ACV, diminished value analysis, demand letter | Minutes to Hours |

| Platinum Report | Total Loss & Legal Support | Comprehensive appraisal, loss of use, expert testimony support | 24-48 Hours |

The Silver Report is a great starting point for those who want a quick estimate. However, for claims involving significant damage or total loss, the Gold and Platinum Reports provide the necessary documentation to reopen underpaid claims. These reports are backed by a money-back guarantee, ensuring that you only pay for a service that delivers tangible value.

Support for Personal Injury and Property Damage Claims

For legal professionals, Vehicle Value Analysis offers specialized bulk solutions. Personal injury firms often focus on bodily injury while leaving property damage claims to be handled separately. This fragmentation can lead to missed compensation for clients and extra work for legal teams.

The WHO OWES WHAT Portal centralizes all property damage work, allowing firms to manage dozens or even hundreds of files with ease. This platform simplifies communication, improves consistency, and saves significant time on every case. It is designed for teams that want to deliver complete representation while navigating complex disputes.

Reports are delivered within 48 hours, ensuring that legal teams have the necessary data to support their clients promptly. The ability to reopen underpaid claims up to two years old provides a powerful tool for recovering lost value for clients who may have accepted low settlements in the past.

Key Takeaways

- Real Data Over Estimates: Vehicle Value Analysis uses verified comparable sales, not algorithmic estimates, to determine pre-loss value.

- Comprehensive Coverage: Services include Actual Cash Value, Diminished Value, and Loss of Use reports for all 50 states.

- Legal Recognition: Reports are recognized by major insurance carriers and supported by over a decade of market data.

- Fast Delivery: Reports are delivered in minutes to 48 hours, depending on the tier selected.

- Law Firm Solutions: Bulk solutions and the WHO OWES WHAT Portal streamline property damage management for high-volume firms.

- Money-Back Guarantee: The service is backed by a $600 money-back guarantee, reducing risk for the consumer.

- Reopening Claims: The firm has the ability to reopen underpaid claims up to two years old, offering a second chance for compensation.

Frequently Asked Questions

What is the difference between Actual Cash Value and Diminished Value?

Actual Cash Value is the value of the vehicle before the accident. Diminished Value is the loss in value that remains after the vehicle has been repaired. Both are critical components of a full property damage claim.

How long does it take to get a valuation report?

Delivery times vary by report tier. The Silver Report is instant. Gold and Platinum Reports are typically delivered within minutes to 48 hours, depending on the complexity of the case.

Can Vehicle Value Analysis help with total loss claims?

Yes. They provide Total Loss Valuation Reports that accurately value challenging insurer assessments. This data is essential for negotiating a fair settlement when the vehicle is deemed a total loss.

Is the diminished value report valid in all states?

Yes, Vehicle Value Analysis provides diminished value coverage and guides for all 50 states. Each state has different laws regarding diminished value recovery, and their reports are tailored to local regulations.

Do you offer services for law firms?

Yes, they offer bulk business solutions and the WHO OWES WHAT Portal for law firms handling multiple motor vehicle personal injury cases. This streamlines the management of property damage claims.

What is the cost of a diminished value report?

The Inherent Diminished Value Report is priced at $199.95. This fee is often recoverable from the at-fault insurance carrier as part of your claim.

Can I reopen an old underpaid claim?

Yes, Vehicle Value Analysis has the ability to reopen underpaid claims up to two years old. This provides a valuable opportunity for clients who may have accepted a low settlement in the past.

Get Your Accurate Valuation Today

Do not accept the first offer from your insurance company. If you believe your vehicle’s pre-loss value was underestimated, Vehicle Value Analysis provides the expert support you need. Visit Vehicle Value Analysis to start your report and recover the compensation you deserve. Their team is ready to help you navigate the complexities of property damage claims with confidence and precision.